Our Stock of the Week is PureCyle Technologies (PCT). PCT is a plastics-recycling company focused on polypropylene, a widely used plastic for packaging, automotive parts, fibers, etc. It uses a proprietary solvent-based purification process that was licensed from Procter & Gamble (PG) to convert polypropylene waste into ultra-pure, “virgin-like” recycled resin sold under the brand name PureFive™.

The PCT process retains the PP polymer, removes contaminants, color, odor, and additives, and produces a resin suitable for a wide range of applications such as food packaging, fibers, thermoforming, and automotive. This is different than the typical recycling process, which uses chemicals to break down the plastic and is environmentally unfriendly.

There is a large addressable market, as PP is among the most widely produced plastics worldwide. Recycling rates are very low, and there is increasing regulatory pressure on the European Union and other governments to increase recycled content.

The company is now operating its first commercial plant in Ironton, Ohio, and is producing resin at scale. It has announced large-scale expansion plans, including a second-generation plant in Augusta, Georgia, with more than 300 million lbs per year capacity, and facilities in Thailand and Belgium, aiming for a total capacity of 1 billion lbs per year by 2030.

PCT’s success depends on feedstock sourcing, plant ramp-up, cost control, and customer adoption of the resin. The recent milestone in revenue from coffee lids, souvenir cups, and detergent bottle caps is confirming the company’s goals. The goal now is to grow volume and improve margins.

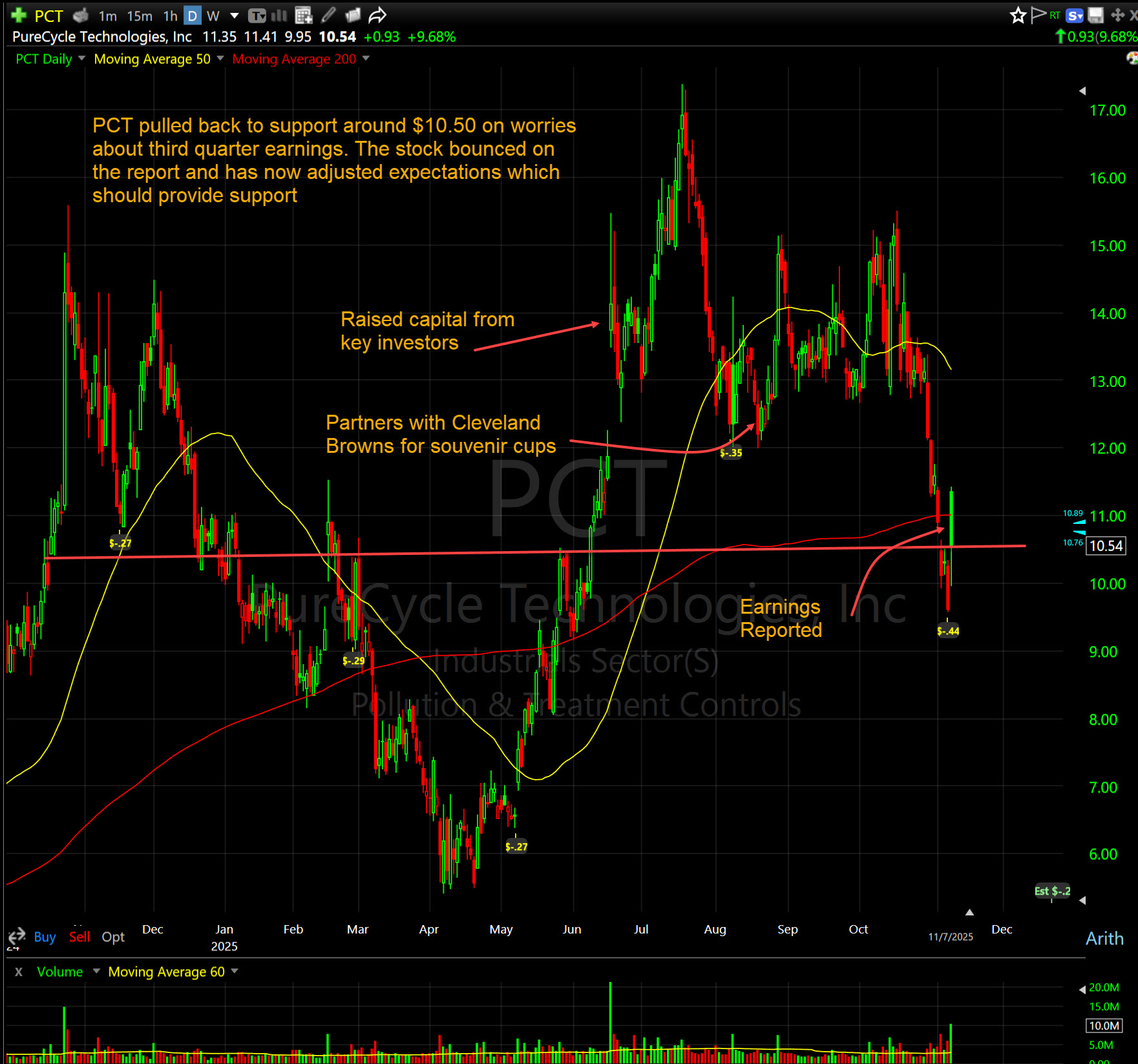

The company has faced execution challenges due to construction delays, regulatory issues, and financing constraints, but has made good progress and is now scaling up revenue. The stock sold off recently due to concerns that it would miss third-quarter revenue expectations. That was indeed the case, but it is now reflected in the stock price.

One reason that PCT has attracted attention is that Stanley Druckenmiller’s Duquesne Family Office reported holding 2,303,084 shares as of June 30. In addition, it also has investments in revenue bonds and convertible preferred shares. While this investment is relatively minor compared to Duquesne’s total assets, it illustrates confidence in the business model.

On October 22, Seaport Research Partners initiated coverage of the stock with a $23 price target, more than double the current price. Seaport is projecting revenues of $526 million as capacity comes online. The analyst cites ‘peerless technology’ and significant underserved demand as the basis for this ‘unique value proposition’.

The stock has been choppy as the company has failed to meet some of its more ambitious goals on time, but it is making progress in commercialization, and those expectations have now been reset after the recent earnings report.

Technically, the stock has support around the $10 to $10.50 area. It jumped on Friday after the report, but faded as some recent holders sold into strength. As always, we will be trading the stock aggressively as it develops.

This post is for educational purposes only! This is not advice or a recommendation. We do not give investment advice. Do not act on this post. Do not buy, sell, or trade the stocks mentioned herein. We WILL actively trade this stock differently than discussed herein. We will sell into strength and buy or sell at any time for any reason. We will actively trade into any unusual activity. At the time of this post, principals, employees, and affiliates of Shark Investing, Inc. and/or principals, clients, employees, and affiliates of Hammerhead Financial Strategies, LLC, directly or indirectly, controlled investment and/or trading accounts containing positions in PCT. To accommodate the objectives of these investing and/or trading accounts, the trading in these shares will be contrary to and/or inconsistent with the information contained in this posting.